How the methodology works

IDC’s research methodology utilizes a comprehensive approach. Every vendor submits to structured questionnaires covering product capabilities, business strategy, go-to-market approach, and innovation roadmap. These assessments leverage the expertise of the IDC team, including senior research analysts who conduct in-depth market and technology research. This is followed by live briefings where IDC analysts probe deeper into each vendor’s positioning.

Critically, IDC doesn’t just take vendors at their word. They conduct direct customer reference interviews to validate claimed strengths and surface real-world challenges. This ensures the assessment reflects actual user experience, not just product promises.

IDC evaluates vendors based on two key metrics:

Capabilities score: Measures what vendors deliver today. This weighs product functionality, data management, AI features, integration options, user experience, customer satisfaction, and also reflects the vendor’s business execution in operationalizing carbon management strategies. It answers the question: can this platform handle your needs right now?

Strategy score: Measures alignment with future customer needs. This evaluates R&D investment, innovation roadmap, market understanding, and positioning for emerging requirements. It answers the question: will this platform still meet your needs in three to five years?

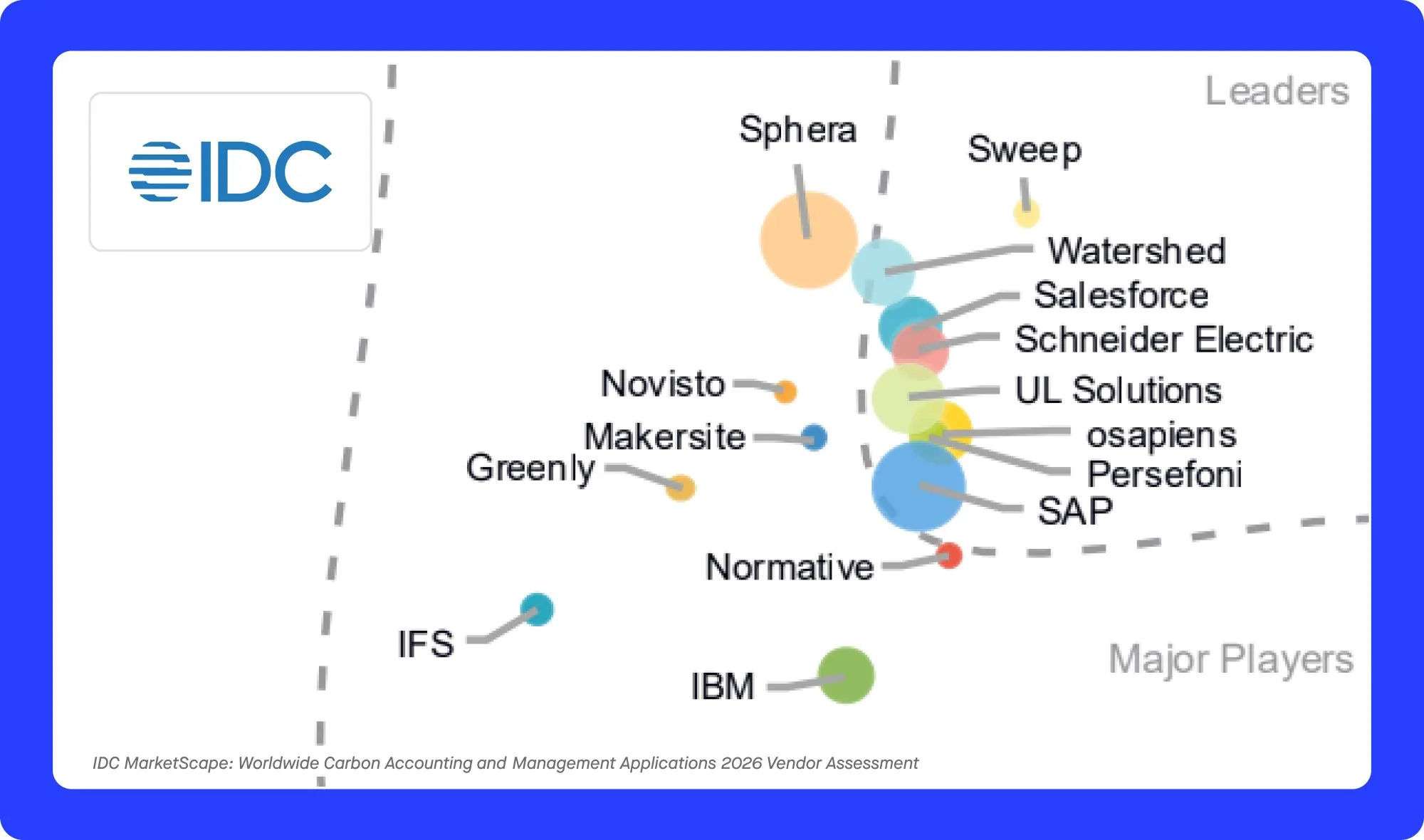

Every vendor is plotted on a graph with capabilities on the vertical axis and strategy on the horizontal axis. Position on this chart determines categorization.

The 2026 assessment results

IDC evaluated 17 vendors for the 2026 carbon accounting MarketScape, placing them into three categories. Each vendor’s position on the IDC MarketScape graph reflects their placement within the given market, visually representing their strategic standing and capabilities.

Leaders (8 vendors): Sweep, Watershed, Persefoni, Salesforce, SAP, Schneider Electric, UL Solutions, osapiens

Major players (8 vendors): IBM (Envizi), Greenly, Normative, Sphera, IFS, Makersite, Novisto, Quentic

Contender (1 vendor): Fujitsu

The Leaders quadrant shows clear segmentation. Some vendors are multi-billion-dollar platforms where carbon management functions as one module within a larger enterprise software ecosystem. Others are pure-play specialists focused exclusively on carbon and sustainability data. Vendor market share is depicted in the IDC MarketScape’s graphical illustration, with the size of each circle highlighting the relative dominance of each vendor in the given market.

AI as a first-class evaluation criterion

One of the most significant developments in the 2026 assessment is how AI capabilities are weighted. AI features, AI governance, AI explainability, and customer assessment of AI impact all factor into vendor scoring, particularly within the strategy assessment.

By 2027, 40% of manufacturers are projected to use AI-driven analytics to optimize energy use, potentially reducing carbon emissions by up to 30%. The vendors scoring highest on AI are those building responsible, auditable intelligence grounded in trustworthy data foundations rather than deploying numerous low-capability agents.

This reflects a broader market maturation. The platforms that succeed aren’t just automating tasks. They’re providing explainable, traceable results that hold up to external audit.

Where the market is heading

The IDC study reveals several clear trends shaping the worldwide carbon management market:

Regulatory compliance is accelerating

Mastering carbon accounting is not about just compliance; it is a strategic imperative that goes beyond just compliance, supporting organizations in building resilience and competitive advantage in an era of escalating environmental scrutiny. Organizations that take action today will reap the business, reputational, and climate benefits tomorrow.

Scope 3 is the battleground

A critical need for robust Scope 3 emissions data collection has been identified, often regarded as the most challenging aspect of carbon accounting for businesses. Scope 3 emissions, which include all indirect emissions that occur in a company’s value chain, are often the largest source of carbon emissions for many organizations, making their management critical for achieving overall sustainability goals. Over 40% of a manufacturer’s carbon footprint can be addressed by transforming supply chain processes, such as sourcing raw materials and optimizing logistics networks.

Data management separates winners from the rest

Centralizing ESG data is essential for organizations to effectively track, manage, and report their sustainability efforts amid evolving regulatory landscapes and stakeholder pressures. There is an increasing need for organizations to adopt platforms that facilitate ESG data centralization to meet compliance and reporting requirements. Vendor platforms are evaluated based on their ability to integrate emissions data across business units, providing a single source of truth for carbon reporting. The vendors scoring highest excel at mapping complex organizational hierarchies: multi-entity, multi-site, multi-subsidiary structures mapped precisely and aggregated at every level.

Solutions in carbon management are evolving from simple reporting tools into integrated, decision-oriented platforms that align carbon tracking with broader operational and decarbonization objectives. The integration of sustainability data into core business processes allows organizations to make informed decisions that align with both financial and environmental goals. About 30% of organizations now purchase sustainability software specifically for strategic differentiation and competitive advantage.

Decarbonization and sustainability goals

Advanced carbon management platforms guide organizations toward net zero by supporting decarbonization strategies and enabling value creation through sustainability initiatives.

Meeting future customer needs

To meet future customer expectations and evolving stakeholder demands, platforms support organizations in adopting advanced carbon management solutions that anticipate regulatory and market requirements.

What the research reveals about vendor differentiation

According to IDC’s assessment, vendors differentiate on several key dimensions:

Enterprise-grade data architecture separates platforms built for scale from those still maturing. The ability to load data once and use it everywhere, with native connectors, real-time APIs, OCR, and SFTP support, determines whether a platform can handle complex enterprise requirements.

Organizational complexity mapping proves critical for large, multi-entity businesses, particularly those with active M&A activity. Not all platforms can accurately model and aggregate emissions across complex corporate structures.

Product carbon footprinting integration is increasingly table stakes. Effective management of Scope 3 emissions requires collaboration with suppliers and stakeholders to ensure accurate data collection and to implement strategies for emissions reduction throughout the value chain. Platforms that handle both corporate and product footprints on a single data ingestion layer score higher than those requiring separate workflows.

Configurability versus simplicity presents an ongoing tension. Some vendors excel at providing deep configuration options for methodology and reporting. Others prioritize out-of-the-box simplicity. The highest-scoring vendors are making sophisticated capabilities simpler through AI assistance, natural-language interfaces, and smarter defaults.

Sweep ranked highest on both capabilities and strategy among all 17 vendors evaluated in the 2026 assessment.

IDC highlighted several specific strengths in Sweep’s assessment. The platform’s skills-based AI approach, which builds fewer, highly capable agents on a trustworthy data foundation rather than deploying dozens of low-capability agents, received particular mention. Customer references validated that Sweep’s AI features hold up to audit requirements, and organizations reported success in achieving compliance, improving financial performance, and advancing sustainability outcomes through the platform.

The platform’s enterprise data management architecture, which maps disparate data formats into a single trusted dataset reusable across reports and decisions, was cited as a key capability differentiator. IDC also called out Sweep’s ability to map complex multi-entity organizational hierarchies and its embedded LCA workflows, with one customer reporting they cut LCA creation time in half while reducing consultant spend. As part of its comprehensive offering, Sweep delivers net zero services, integrating emissions data, decarbonization strategies, and transition planning to help clients achieve their net-zero goals.

This represents a four-year progression. In 2023, Sweep wasn’t assessed in the IDC MarketScape. By 2024, it was named a Leader. In 2025, it moved to the tip of the Leaders quadrant. The 2026 assessment shows continued momentum, with the highest positioning on both axes.